1.2.4 Price

In this lesson, we will explore the meaning of price, its relationship with resource distribution, equilibrium price and quantity, the interaction of demand and supply, the role of markets in price determination and resource allocation, and how market forces of demand and supply affect equilibrium price and quantity.

Price

Price refers to the monetary value assigned to a good or service in the marketplace. It represents the amount of money or other forms of compensation that buyers are willing and able to pay to acquire a particular product or service.

Price reflects the perceived worth or value of a good or service in the eyes of buyers and sellers. It considers factors such as production costsThe sacrifices made when choosing a particular option, which may include money spent, time used, or resources consumed., supply and demand dynamics, consumer preferencesWhat customers want, value, and expect from products and services., scarcityThe situation where limited resources are not sufficient to satisfy unlimited human wants., and market competition.

Prices play a crucial role in resource allocation as they influence producers' decisions on what to produce, how much to produce, and how resourcesThe inputs used to produce goods and services, including the factors of production. should be allocated. Prices guide the efficient distribution of resources by signalling the relative scarcity or abundance of goodsPhysical, tangible products that can be touched and stored. and servicesIntangible products that provide a skill, experience, or benefit rather than a physical item. in the market.

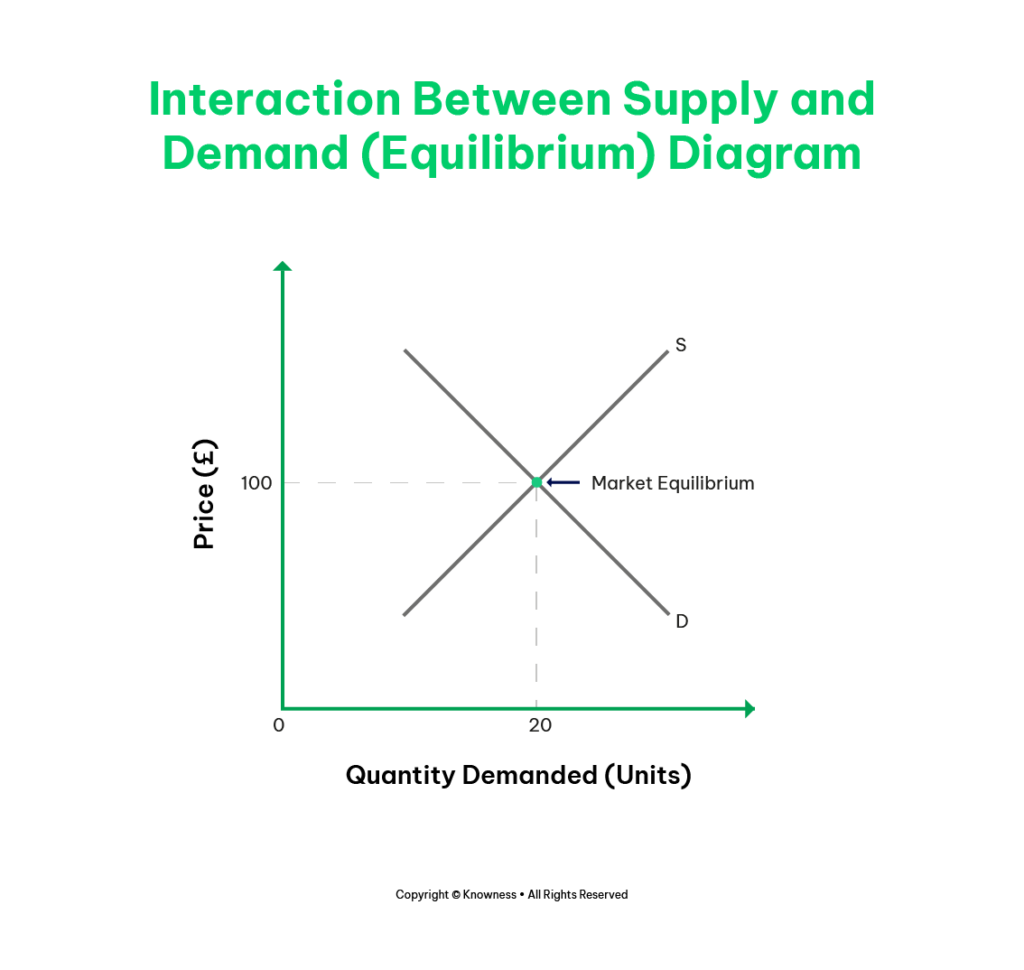

Equilibrium Price and Quantity

Equilibrium Price: Equilibrium price, also known as market-clearing price, is the price at which the quantity demanded by consumersIndividuals or households that buy and use goods and services to satisfy their needs and wants. equals the quantity supplied by producersBusinesses or organisations that combine resources to produce goods and services for consumers.. It is the point of balance between supply and demand, where there is neither excess supply nor excess demand.

Equilibrium Quantity: Equilibrium quantity is the quantity of a good or service that is bought and sold in the market at the equilibrium price. It represents the quantity at which buyers and sellers agree upon in the marketplace.

Interaction of Demand and Supply

Demand represents the quantity of a good or service that consumers are willing and able to buy at various prices, while supply represents the quantity of a good or service that producers are willing and able to provide at different prices. The interaction of demand and supply determines the equilibrium price and quantity in the marketplace.

The demand curve illustrates the relationship between price and quantity demanded, while the supply curve depicts the relationship between price and quantity supplied. By analysing the interaction of these curves, we can determine the equilibrium price and quantity.

Role of Markets in Price Determination and Resource Allocation

Markets serve as platforms or mechanisms where buyers and sellers interact to exchange goods, services, and resources. Through the forces of supply and demand, markets determine the equilibrium price and quantity.

Markets play a crucial role in allocating resources efficiently. When prices adjust to equilibrium levels, they provide signals to producers about the scarcity or abundance of goods and services. Producers respond by allocating resources towards the production of goods and services that are in high demand, resulting in an efficient allocation of resources.

Market Forces and Equilibrium

Market forces of demand and supply influence the equilibrium price and quantity. Changes in demand or supply can lead to shifts in the demand or supply curve, resulting in changes in the equilibrium price and quantity.

- Changes in Demand: An increase in demand leads to a higher equilibrium price and quantity, while a decrease in demand leads to a lower equilibrium price and quantity.

- Changes in Supply: An increase in supply leads to a lower equilibrium price and a higher equilibrium quantity, while a decrease in supply leads to a higher equilibrium price and a lower equilibrium quantity.

Conclusion

Price reflects the worth of goods and services and guides resource allocation decisions. Equilibrium price and quantity represent the balance point where supply meets demand. Markets serve as the mechanism for determining price and facilitating resource allocation. The forces of demand and supply interact to shape the equilibrium price and quantity.